Debt can be a very scary thing. If you are not careful, before you know it you have mounds of debt laying at your feet. How can you handle it if you end up creating more than you can handle? Here are a few steps to help you get back on your feet.

Make more than the minimum payment. Credit card companies love it when you pay just enough to get by every month. At that rate, you’re mostly paying off interest and barely scratching the surface of your actual debt. You will want to pay more than what they are asking for in order to decrease payments and minimize those monthly accruing interest charges. Pay off debt with the highest interest rate first. It goes almost without saying, but it’s something that a lot of people forget. If one credit line is charging you 11% APR (interest over the course of a year) while another credit line is charging you 9% APR, focus all your attention on the debt that falls under 11% interest rate. Pay it off before even touching the other debt. You want to pay off the one with the highest interest rate in order to decrease your interest debt. Sure the other cards will continue to charge interest but it will be at a lower rate, and in return not charge you as much as a higher rate in the long run. Talk to your credit card companies. Explain your financial situation and ask if there is anything they can do to help. Many will lower your interest rate for a period of time and/or waive current late fee balances, to give you a better opportunity to catch up. Especially if you are one that has never had a history of late fees and or credit problems in the past. Never close cards with existing balances. It might seem like an easy way to get a handle on your debt, but it’ll do horrors to your credit score, and you’ll still be on the hook for the debt. All this will do is send your credit utilization (your available limit v. your current debt) down, further driving down your credit score. Learn more here on how to increase your credit score. Move your debts around. Though transferring money from a credit card with 12% interest to a card with 0% interest may damage your short-term credit, barely chipping away at your debt because your interest is so high will damage your finances in the long term. Shop around for long-term, low- or no-percent interest rate transfer opportunities, or look into transferring some of your debt onto a low-interest card that you already have. Keep the following in mind: How long the low interest rate will last. Depending on your total debt and how quickly you think you can pay it off, 0% interest for six months may not be as good a deal as 2% for 18 months. Liquidate big ticket items to help lower your debt. If you just bought a car, or a memory foam mattress, or a new dirt bike, think seriously about your ability to keep such big-budget items, especially if you’re paying for them on installment. Liquidating your big-ticket items now will mean less financial hardship for you later on. This is one not everyone likes to do, but if you are in a bind it’s better to wait and re buy an item later when you are in a more stable financial situation than to have an item and have headaches continuously over debt each month.

Needing more help? Have more questions about credit? At Texas Premier Mortgage, we have licensed loan officers who specialize in helping people to be able to afford their home whether it be right away or in the future. They can help sort through your debt and offer assistance as needed. Why not give them a call today so they can help you decrease your debt so you can afford that dream home you have always wanted. Contact Steve Head, President of Texas Premier Mortgage to begin your steps to decreasing your debt and gaining that perfect home.

Many factors come into play once you decide you are ready to take the next step: applying for the mortgage. It sounds really scary to one who has not ever had any experience with owning their own home. With a knowledgeable lender who can lead you each step of the way there really is nothing to worry about at all! A few things that will need to be looked at. The lender will want to see financial stability. A potential lender will look for steady employment, with a single employer for the past two years or at least employment in the same field. Your credit history and if you have any late note payments will also be a factor. Lenders pay particular attention to any rent or mortgage payments that were more than 30 days past due. They will also look into your current bank statements. In order to qualify for a mortgage, most lenders require that you have a debt-to-income ratio of 28/36. This means that no more than 28 percent of your total monthly income (from all sources and before taxes) can go toward housing, and no more than 36 percent of your monthly income can go toward your total monthly debt (this includes your mortgage payment). Lenders will ask you to provide some of the following information as well: Your current credit report. Pay stubs for the past 30 days. W-2 forms for the past two years. Information about debt obligations, including car loans, student loans, tax liabilities, liens (including federal tax liens), bankruptcies, etc. Recent statements from your checking, savings, mutual fund or other accounts. Tax returns for the past two years if you’re self-employed. Proof of any supplemental income. Records of any negative credit accounts that have been paid off. Records of child support or alimony if applicable. At Texas Premier Mortgage, we are here to assist you with every step of the process. Contact Steve Head

today at 281-627-4222 to help you begin your journey to purchasing your next home!

Many factors come into play once you decide you are ready to take the next step: applying for the mortgage. It sounds really scary to one who has not ever had any experience with owning their own home. With a knowledgeable lender who can lead you each step of the way there really is nothing to worry about at all! A few things that will need to be looked at. The lender will want to see financial stability. A potential lender will look for steady employment, with a single employer for the past two years or at least employment in the same field. Your credit history and if you have any late note payments will also be a factor. Lenders pay particular attention to any rent or mortgage payments that were more than 30 days past due. They will also look into your current bank statements. In order to qualify for a mortgage, most lenders require that you have a debt-to-income ratio of 28/36. This means that no more than 28 percent of your total monthly income (from all sources and before taxes) can go toward housing, and no more than 36 percent of your monthly income can go toward your total monthly debt (this includes your mortgage payment). Lenders will ask you to provide some of the following information as well: Your current credit report. Pay stubs for the past 30 days. W-2 forms for the past two years. Information about debt obligations, including car loans, student loans, tax liabilities, liens (including federal tax liens), bankruptcies, etc. Recent statements from your checking, savings, mutual fund or other accounts. Tax returns for the past two years if you’re self-employed. Proof of any supplemental income. Records of any negative credit accounts that have been paid off. Records of child support or alimony if applicable. At Texas Premier Mortgage, we are here to assist you with every step of the process. Contact Steve Head

today at 281-627-4222 to help you begin your journey to purchasing your next home!

What drives you?

What drives you? This is a question many people ask themselves but do not ask others. Life brings obstacles but the question is: how do you handle those obstacles? Do you turn the other way and pretend your problem does not exist? Do you hope that it will end in a happy ending? Life is too short….you have to plan ahead! But what keeps you going? Remember this: God won’t bring you through something that he can not help you out of. Whatever he gives you he can bring you through. Things happen. Life may bring you through tough things, but you will come out better and brighter than before if you just have trust and faith. So it is easy to say that. But can we really get out of our problems? Can things really turn around? God will bring you through, you just have to push through your difficulties, keep moving forward, and keep praising God through it all! At Texas Premier Mortgage, we have built our foundation on the premise that if you put God first, and praise him through all things, then everything will fall into place. That is why we continue doing what we do…helping those who need assistance. This year we have reached out to the community, and have been involved with Montgomery County’s Women’s Council of Realtors Community Outreach program that does just that. The Holidays for Heroes program has helped to benefit Veterans for the past nine years. This year we collected items to fill over 500 stockings to be delivered to 40 deployed veterans, and over 400 homeless veterans in Houston that will be hand delivered on Christmas Eve. We also are pleased to announce this year we added a partnership with Lone Star College to create an endowment for a scholarship for veterans returning to school after returning home. This endowment will be ongoing, and what a difference it could mean to a veteran determined to finish college to help continue an abundant life for them. Giving back, that is what it is about, that is what we are about…helping to increase others and lift them up. At Texas Premier Mortgage, we have seasoned loan officers that can help you through your big or small obstacles. It may take some time

but we know it will work our for good. We can walk you through your life’s challenges. No matter where you are, we can help you at any stage of your life. If you need credit assistance we can help. Our highly qualified and seasoned loan officers can assist you through the home loan process. It does not have to be stressful, we can help! Let us know how we can assist you. It is our pleasure. Contact Steve Head today to get started at steve@txpremiermortgage.com, 281-627-4222 or 281-907-6401 ext. 100. We are ready to help!

Are There Lender Options for New Home Construction?

When buying a new home there is a lot to think about. What area do you want to live in? What schools are important to you for your children? Do you have a realtor? All of these questions get answered as you begin your new home search. However, once you find that new home and it is new construction, the question arises: Do I have to purchase through the builder’s lender? Home builders do offer in house lending. You are usually given a list of lenders whom the builder recommends to use. But are these a good deal? One incentive to using their suggested lender is convenience. It is a one stop shop per say. Because the affiliated lender is intimately familiar with the builder, the two companies can share information which can help to speed up the lending process. Some builders offer substantial incentives from reducing the price of the home to upgrading appliances. However, while builders offer these incentives, they are required by federal law to allow homebuyers to obtain their mortgage from any company they choose. They may be able to insist you seek mortgage pre-approval from one of their affiliates as a type of credit check, but they cannot compel you to borrow money from these lenders. So with that being said, yes you are free to shop around and choose your own lender. According to the National Association of Mortgage Brokers (NAMB), affiliated lenders tend to offer interest rates one-eighth to one-quarter percent higher than what consumers could get from an independent lender. Therefore it would be a good idea to check out different companies just to be sure you are getting the best interest rate. You can also experience less options on the type of mortgage that best fits your needs. There is enormous variety in the types of mortgages available today. Not only can homebuyers choose between a fixed-rate or adjustable-rate loan and select their term and payment options, but they can also explore a number of non-traditional mortgages designed for people with specific needs. A builder’s shortlist of partner lenders is unlikely to match the array of mortgages you’ll find if you search for your loan independently. Just as you make a careful search for the right house, it’s worth taking the time to shop around for the best mortgage. Look at what the builder is offering, but compare it with quotes from at least three outside lenders. By considering all of your options, you’ll be able to arrange financing that best suits your needs.

Contact Texas Premier Mortgage today to speak to highly qualified lenders who can work hard to get you the lowest interest rate, and guide you each step of the way for the purchase of your new home.

Private mortgage insurance (PMI) is a type of insurance policy that protects lenders from the risk of default and foreclosure, allowing buyers who are unable to make a significant down payment to obtain mortgage financing at affordable rates. If you purchase a home and put down less than 20%, your lender will minimize its risk by requiring you to buy insurance from a PMI company prior to signing off on the loan. As the borrower, you end up paying the PMI premiums but your lender is the sole beneficiary. If you have monthly PMI, you continue to make PMI payments every month until your PMI is either terminated (when your loan balance is scheduled to reach 78% of the original value of your home); when it is cancelled at your request because your equity in the home reaches 20% of the purchase price or appraised value (your lender will approve a PMI cancellation only if you have adequate equity and have a good payment history); or when you reach the midpoint of the amortization period (a 30-year loan, for example, would reach the midpoint after 15 years). Borrowers usually have to pay PMI when any single loan accounts for more than 80% of the appraised home value. The key word here is “single.” But what if you used two separate mortgage loans to pay for the house? This is a common strategy used by home buyers who have less than 20% saved up for a down payment. For example, you could use an 80-10-10 mortgage to buy a house, and you wouldn’t have to pay for a PMI policy. Here’s what those numbers represent: • 80 = The first mortgage would cover 80% of the purchase price. • 10 = The second home loan (also called a “purchase money second”) would cover 10% of the price. • 10 = You, as the borrower, would pay the remaining 10% out of pocket as a down payment. In this “piggyback” financing scenario, no single loan accounts for more than 80% of the price. Therefore, you wouldn’t have to pay for PMI protection, even though you are putting less than 20% down on the home purchase. How can you avoid paying PMI? You can avoid paying PMI by making a down payment that is at least 20% of the purchase price of your home. There are many ways to consider but it is also a good idea to talk to someone in the mortgage industry who has knowledge regarding this type of insurance. Contact Steve Head, President and owner of Texas Premier Mortgage at 281-627-4222. Available 7 days a week, he is highly educated on this and many other mortgage concerns you may have.

When you are in the market to buy a new home, several factors come to mind. First and foremost you need to figure out your home buying budget. Next, find an area in which you would like to live in. Whether it be in the city, suburbs, or country, there is a place for everyone to find their perfect fit. Once you have your area picked out, you begin your search. Websites such as har.com offer you a vast array of choices as well as multiple sites out there. Make a list of your “must haves” that will help you with your search. Narrow it down to your favorite two or three. Find a local realtor on realtor.com, or har.com to help you with your search. Ask friends, neighbors who they have used in the past or if they can refer you to someone. You will also need a mortgage lender. They are your strongest link between your realtor and your financial institution granting you the money for your loan. When shopping for a mortgage lender make sure they have been in business for at least five years, and you will want someone who has experience with the mortgage field. At Texas Premier Mortgage, we provide top notch customer service and treat our clients as if they were our own family. That is why it is important to find a mortgage broker who knows the ends and outs of the mortgage process, and who constantly educates themselves with the latest and greatest up to date mortgage information possible. Our communication goes beyond the normal “9-5″ persona you may find with other lenders or when dealing with a bank. A member of the Better Business Bureau since 2010 A+ rating, and the winner of the 2014 BBB Excellence award, we strive to provide the utmost excellence when helping our clients obtain their home buying goal. Steve Head, President of Texas Premier Mortgage since 2006, has vast experience and knowledge to help be your strongest link in the home buying process. He knows all the current up to date mortgage news, has the experience most new loan originators lack, and has lived in The Woodlands, TX area for most of his life. Therefore he knows the area very well, and can help assist you with any questions you may have. Contact Steve Head with Texas Premier Mortgage today at 281-627-4222, or email at steve@txpremiermortgage.com. Let us help you by becoming Your Mortgage Lender, Your Strongest Link.

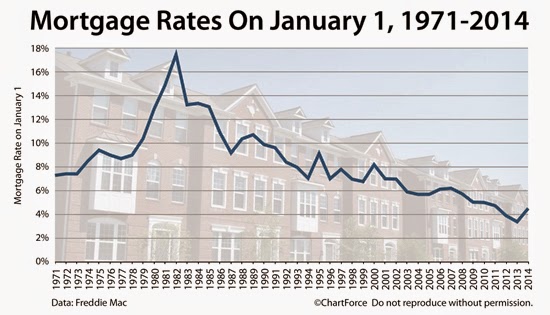

One of the most important aspects to successfully obtaining a mortgage is securing a low interest rate. After all, the lower the rate, the lower the payment each month. Unfortunately, many homeowners tend to just go along with whatever their bank or mortgage broker offers, often without researching mortgage lender rates or inquiring about how it all works. Whether you’re interested in rates or not, it’s wise to get a better understanding of how mortgage rates move and why. To put it in perspective, a change in rate of a mere .125% (eighth percent) or .25% (quarter percent) could mean thousands of dollars in savings or costs annually. And even more over the entire term of the loan. So what can determine the mortgage rates? 1. Treasury Bonds. The 10-year Treasury bond yield is said to be the best indicator to determine whether mortgage rates will rise or fall. Typically, when bond rates (also known as the bond yield) go up, interest rates go up as well. And vice versa. Investors turn to bonds as a safe investment when the economic outlook is poor. When purchases of bonds increase, the associated yield falls, and so do mortgage rates. But when the economy is expected to do well, investors jump into stocks, forcing bond prices lower and pushing the yield (and mortgage rates) higher. 2. Economic activity. As a rule of thumb, bad economic news brings with it lower mortgage rates, and good economic news forces rates higher. Remember, if things aren’t looking too hot, investors will sell stocks and turn to bonds, and that means lower yields and interest rates. If the stock market is rising, mortgage rates probably will be too, seeing that both climb on positive economic news. And don’t forget the Fed. When they release “Fed Minutes” or change the Federal Funds Rate, mortgage rates

can swing up or down depending on what their report indicates about the economy. Generally, a growing economy (inflation) leads to higher mortgage rates and a slowing economy leads to lower mortgage rates. Inflation also greatly impacts mortgage rates. If inflation fears are strong, interest rates will rise to curb the money supply, but in times when there is little risk of inflation, mortgage rates will most likely fall. 3. Freddie Mac’s weekly mortgage rate survey. Freddie Mac’s average mortgage rates are updated weekly every Thursday morning. Since 1971, Freddie Mac has conducted a weekly survey of mortgage rates. These are averages gathered from banks throughout the nation for conventional (non-government) conforming mortgages with an LTV ratio of 80 percent. The numbers are based on quotes offered to “prime” borrowers, meaning best-case pricing for the most part. As you can see, 30-year fixed mortgage rates are the most expensive relative to the 15-year fixed and select adjustable-rate mortgages. This is the case because the 30-year fixed rate never changes, and it’s offered for a full three decades. So you pay a premium for the stability and lack of risk. Rates on the 15-year fixed are significantly cheaper, but you get half the time to pay it off, meaning larger monthly payments. Rates on ARMs are discounted at the outset because you only get a limited fixed period before they become adjustable, at which point they generally rise. For more information and further explanation contact Steve Head, President of Texas Premier Mortgage at 281-907-6401 ext. 100.

When you’re buying a home using a mortgage, refinancing your existing mortgage, or selling your home to anyone other than an all-cash buyer, the home appraisal is a key component of the transaction. Whether you’re a buyer, owner or seller, you’ll want to understand how the appraisal process works and how an appraiser determines a home’s value. An appraisal is an unbiased professional opinion of a home’s value. Appraisals are almost always used in purchase and sale transactions and commonly used in refinance transactions. In a purchase and sale transaction, an appraisal is used to determine whether the home’s contract price is appropriate given the home’s condition, location and features. In a refinance, it assures the lender that it isn’t handing the borrower more money than the home is worth. Lenders want to make sure that homeowners are not over borrowing for a property because the home serves as collateral for the mortgage. If the borrower should default on the mortgage and go into foreclosure, the lender will recoup the money it lent by selling the home. The appraisal helps the bank protect itself against lending more than it might be able to recover in this worst-case scenario. When you’re buying a home and you’re under contract, the appraisal will be one of the first steps in the closing process. If the appraisal comes in at or above the contract price, the transaction proceeds as planned. If the appraisal comes in below the contract price, however, it can delay or derail the transaction. If you’re refinancing a conventional mortgage, a low appraisal can prevent you from refinancing your home. The home needs to appraise at or above the amount you want to refinance for your loan to be approved. However, if your existing mortgage is an FHA mortgage, you can refinance without an appraisal through the FHA Streamline program. FHA Streamline is a great option for underwater homeowners. Contact the Texas Premier Mortgage team to find out more, and to help you through the home loan process.